By [email protected]

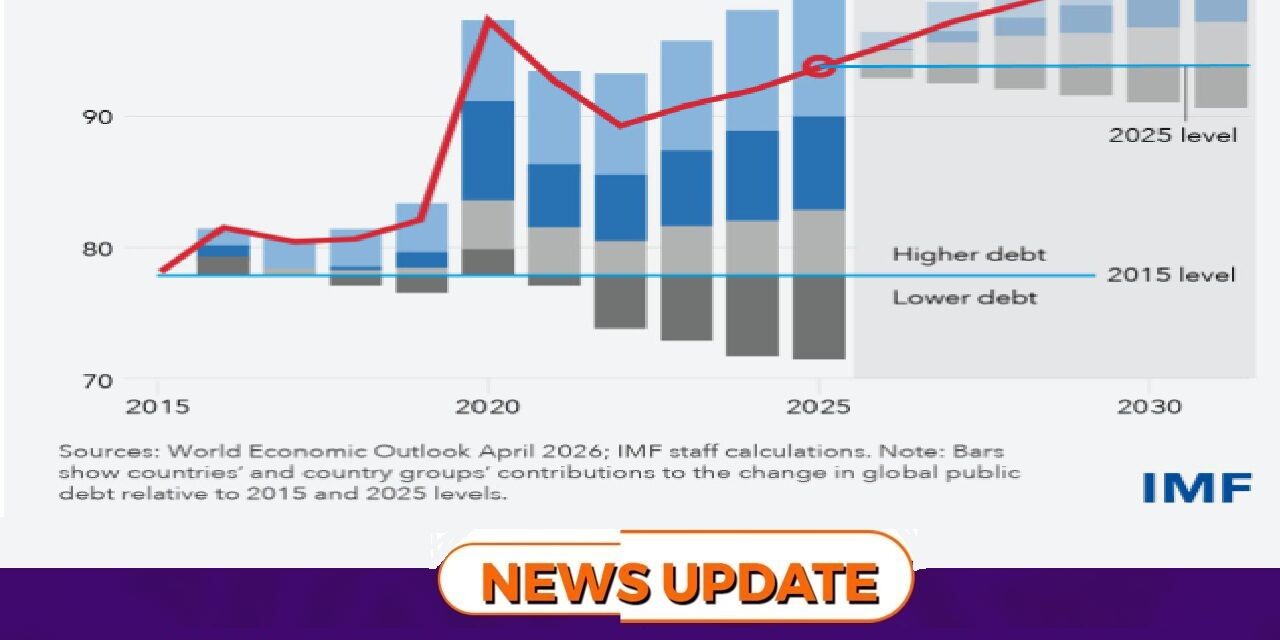

Freetown, 16th April, 2026 – The world’s debt burden is climbing to historic levels, with the International Monetary Fund (IMF) warning that global public debt is projected to reach 100 percent of GDP by 2029. Economists say relying on economic growth alone to ease the strain is a risky gamble.

According to the IMF’s World Economic Outlook released this month (April), global debt surged sharply during the pandemic years, dipped slightly, but is now on a steady upward trajectory. By 2030, debt levels are expected to surpass the 2015 baseline by a wide margin, driven largely by the United States, China, and a cluster of emerging economies.

The report highlights that while advanced economies continue to borrow heavily to finance social programs and infrastructure, many developing countries are struggling with debt sustainability, facing higher borrowing costs and weaker fiscal buffers.

“Waiting for growth alone to do the work is a risky proposition,” the IMF cautioned, noting that without decisive fiscal reforms, debt vulnerabilities could undermine global financial stability.

Experts argue that governments must balance growth strategies with credible debt management plans, including expenditure controls, revenue mobilization, and structural reforms. For countries like Sierra Leone, where debt servicing already consumes a significant share of public revenue, the warning underscores the urgency of tightening fiscal discipline while safeguarding social spending.

With global debt inching toward the symbolic 100 percent threshold, the IMF’s message is clear: the time for proactive debt management is now.