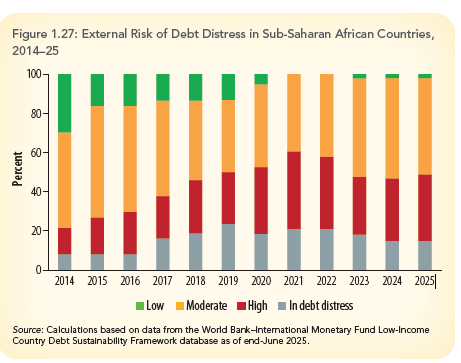

Freetown 13th October 2025– Sub-Saharan Africa is facing a mounting fiscal crisis, with the number of countries in or approaching debt distress surging from eight in 2014 to twenty-three in 2025 nearly half the region. This sharp rise reflects a decade of crisis-era borrowing, sluggish revenue growth, and increasing dependence on costly non-concessional loans.

The financial strain is most evident in external debt servicing, which now consumes 2 percent of the region’s GDP more than double the share recorded a decade ago. This growing burden is crowding out essential public spending, particularly in health, education, and infrastructure, and placing governments under intense budgetary pressure.

Despite these headwinds, the region’s economy is showing signs of cautious recovery. GDP growth is projected to edge up to 3.8 percent in 2025, from 3.5 percent in 2024, driven by easing inflation and a gradual rebound in investment. Inflationary pressures have notably declined, with the number of countries experiencing double-digit inflation falling from twenty-three in late 2022 to just ten by mid-2025.

However, this fragile progress is vulnerable to external shocks. Uncertainty in global trade policy, waning investor confidence, and shrinking access to international financing continue to pose significant risks to the region’s economic outlook.

Beyond cyclical challenges, a deeper structural issue looms: Sub-Saharan Africa is undergoing the world’s largest demographic transformation. Over the next 25 years, the working-age population is expected to grow by more than 600 million. Yet only 24 percent of new entrants to the labor market currently secure wage-paying jobs, raising concerns about future employment and social stability.

“The challenge will be matching this growing population with better jobs,” said Andrew Dabalen, Chief Economist for the Africa Region at the World Bank. “A structural shift toward more medium and large firms is essential to generate wage jobs at scale.”

The World Bank’s latest Africa’s Pulse report outlines a roadmap for economic transformation. Key recommendations include reducing the cost of doing business, expanding access to energy, digital services, and transport infrastructure, and investing in human capital. Governance reforms and stronger institutions are also critical to attracting private investment and unlocking sustainable growth.

Sector-specific strategies offer promising avenues. Agribusiness, mining, tourism, and housing are identified as high-potential industries for job creation. In tourism alone, every direct job generates an additional 1.5 related jobs, underscoring the sector’s multiplier effect.

While the region’s resilience remains a bright spot, the twin challenges of rising debt and a looming employment crisis demand urgent and coordinated policy action. Without bold reforms, current growth levels will fall short of lifting millions out of poverty or harnessing the full potential of Africa’s expanding workforce.